India’s digital economy does not slow down between news cycles. While the country’s technology story is often told through the lens of startup funding rounds, government policy announcements and the quarterly results of its largest listed tech companies, the more consequential changes happen at the user level — in the habits, preferences and expectations of the hundreds of millions of Indians who go online every day. In 2026, those habits are shifting in ways that are creating clear winners and losers among the platforms competing for attention and spending. Platforms like https://topx-site.com/ — running on PWA technology, accepting PhonePe, PayTM and UPI in INR, and offering a Hindi-language interface alongside English — illustrate precisely the kind of localisation depth that separates platforms gaining traction in India from those that remain perpetually on the margins.

The Attention Economy Gets More Competitive

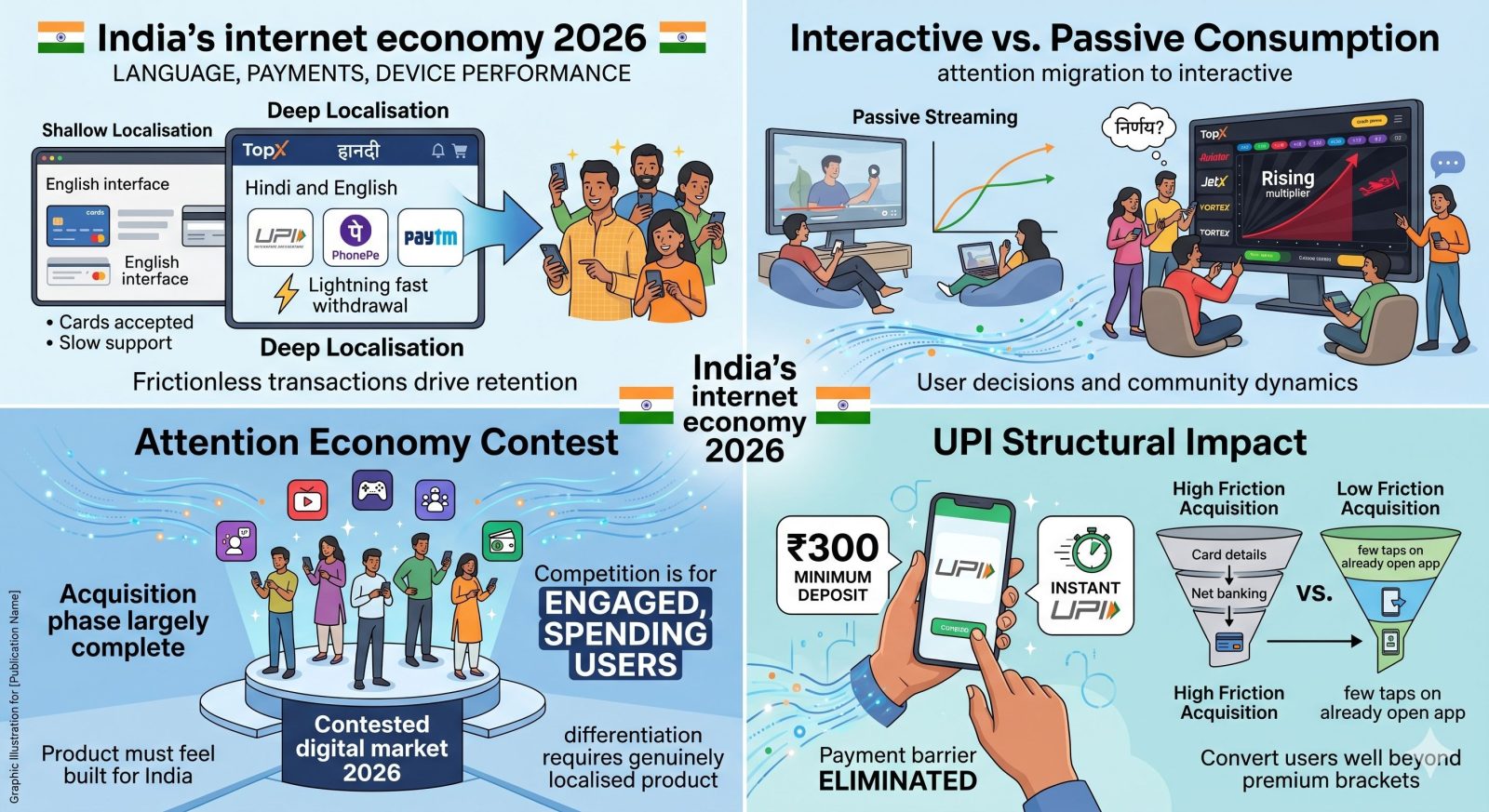

India added more internet users in the past three years than most countries have in total. That growth has made it one of the world’s most contested digital markets, but it has also changed the nature of the competition. The early phase of India’s internet growth was about acquisition — getting users online for the first time, getting them to download apps, getting them to make a first digital transaction. That phase is largely complete in urban India and well advanced in Tier-2 and Tier-3 cities.

The competition now is for engaged, spending users — people who are already online, already comfortable transacting digitally, and choosing between a growing array of products that all meet a basic threshold of functionality. In that environment, differentiation requires more than a working product. It requires a product that feels genuinely built for India, not adapted from somewhere else as an afterthought.

Why Localisation Depth Determines Outcomes

The phrase “localised for India” covers a wide spectrum of actual effort. At the shallow end, it means an English interface with INR pricing. At the deep end, it means Hindi and regional language support, UPI and PhonePe as primary payment methods rather than secondary ones, customer support that operates in languages users actually speak, and a product architecture that performs well on the mid-range Android devices that represent the majority of India’s installed hardware base.

The difference between shallow and deep localisation shows up most clearly in retention data. Users who encounter a product that handles their language, their payment method and their device class without friction are substantially more likely to return. Users who have to switch to English to complete a transaction, or whose preferred payment method is buried three menus deep, are users who are one bad experience away from churning permanently.

The Rise of Interactive Formats

One of the clearest signals in India’s digital behaviour data in 2026 is the continued migration of attention from passive content consumption toward interactive formats. Streaming growth has moderated. The categories accelerating are those where the user makes decisions, takes actions and experiences outcomes that vary based on their choices.

Crash games represent the most visible expression of this trend in the online entertainment space. Titles like Aviator, JetX and VORTEX — where a multiplier climbs in real time and the user must decide when to cash out — have built audiences across India that cut across geographic and demographic lines. The format is brief enough to fit into the fractured leisure windows of a working day, transparent enough to feel fair, and social enough — many titles show other users’ activity in real time — to generate the community dynamics that sustain long-term engagement.

What UPI Made Possible Beyond Payments

UPI’s impact on India’s digital economy is routinely framed in terms of payment volumes and transaction counts. The more interesting story is what UPI made possible structurally — specifically, the elimination of payment as a meaningful barrier to digital product adoption. When a new user can complete their first transaction on a platform in under thirty seconds, using an app already installed on their phone, the entire economics of digital user acquisition change.

Platforms that understood this early built their growth models around it. Low minimum transaction thresholds — deposits from ₹300, accessible to users well beyond the premium income brackets — combined with instant UPI processing created acquisition funnels that convert at rates the previous generation of payment infrastructure simply could not support.

The Platforms That Will Define the Next Phase

India’s digital economy in 2026 is past the point where being present in the market is sufficient. The platforms that will define the next phase of growth are those that have solved the full stack of localisation — language, payments, device performance and cultural relevance — and built operational infrastructure capable of serving a user base that is large, geographically diverse and increasingly sophisticated in its expectations. That bar is higher than it was three years ago, and it is rising.